Rightmove plc

Rightmove is a highly profitable “toll bridge” for the UK property market with excellent returns on capital, but it currently has to defend its dominant stronghold against an aggressive, well-funded attacker.

Summary

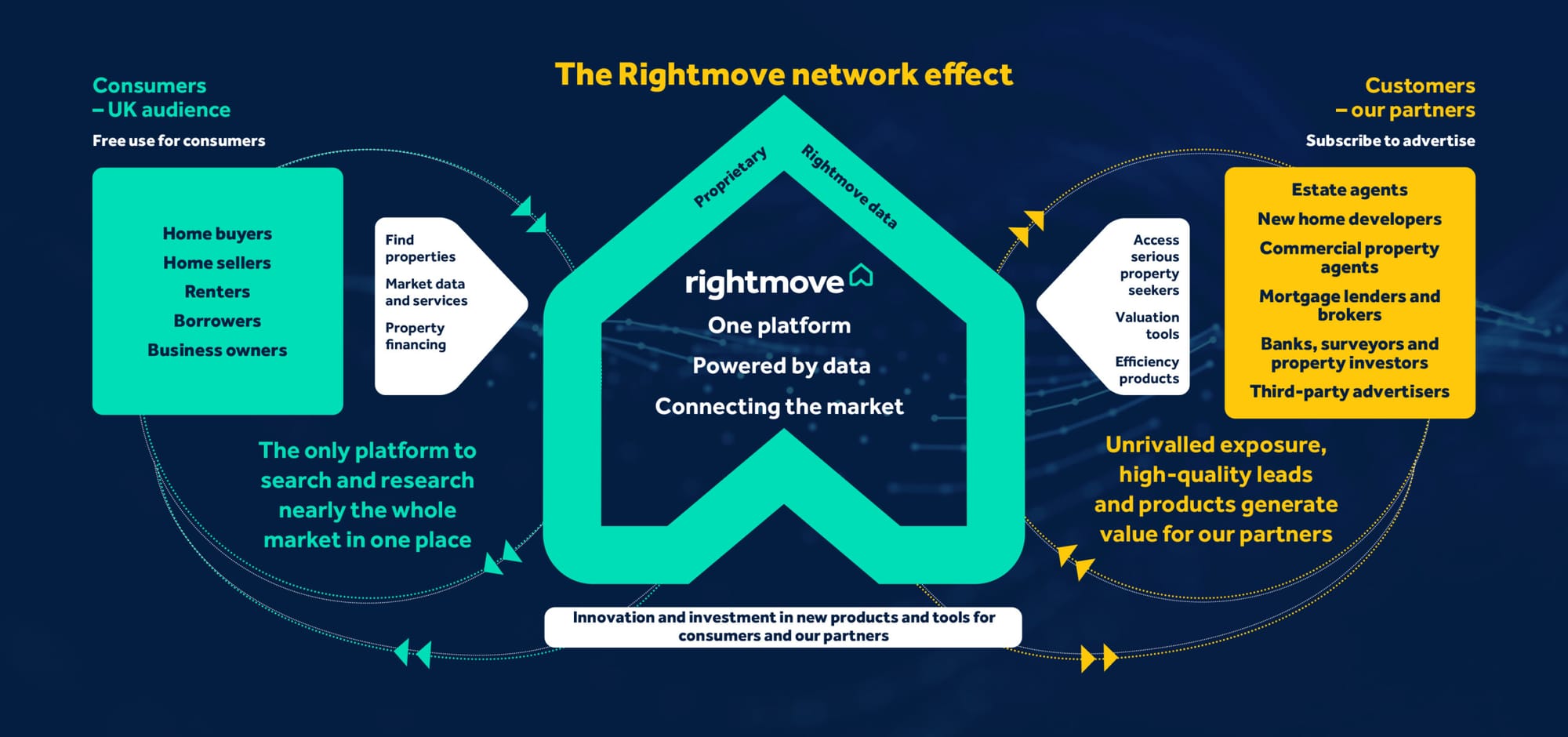

Rightmove plc is the undisputed market leader in digital real estate marketing in the United Kingdom and is a classic example of a platform company with extremely strong network effects. The company aggregates the most comprehensive inventory of properties for sale and rent, attracting the largest number of users looking to buy and rent, which in turn forces real estate agents and developers to be present on the platform. This “winner-takes-most” model has historically provided Rightmove with operating margins of over 70% and exceptionally high cash conversion, as the business model traditionally requires only low capital investment. The company primarily earns its money through monthly subscription fees from real estate agents and developers, supplemented by revenue from strategic growth areas such as commercial real estate, mortgage brokerage, and data services.

Economically, the company is extremely robust, with a debt-free balance sheet and strong free cash flow, which is consistently returned to shareholders through dividends and share buybacks. The latest financial data from the first half of 2025 confirms the resilience of the model, with revenue growth of 10% and a stable customer base, even in a challenging macroeconomic environment.1 Nevertheless, Rightmove is at a strategic turning point. The entry of the well-capitalized US-based CoStar Group into the UK market through its acquisition of OnTheMarket has significantly increased the intensity of competition. This is forcing Rightmove to increase its investments in technology (AI, cloud migration) and marketing, which could put pressure on margin expansion in the short to medium term.

The key advantages lie in the deeply established brand, user habits, and high switching costs for brokers, who cannot afford to leave the platform. The risks are concentrated on the potential erosion of market share by CoStar and technological disruptions in search behavior. For investors, the question arises as to whether the current valuation discount overcompensates for the competitive risks or whether a structural revaluation of earnings power is necessary.

1. What they sell and who buys it

Products and services

Rightmove does not sell real estate, but rather attention, data, and efficiency. The company acts as a two-sided marketplace that brings together supply (real estate inventory) and demand (buyers/tenants). Its products can be divided into three main categories:

The core product: listings and visibility

The fundamental offering is real estate listings. Real estate agents and developers pay to have their properties appear on Rightmove's website and mobile app. Since Rightmove accounts for over 80% of total user time on British real estate portals, this visibility is not optional but mission-critical for the business success of real estate agents.5 Without a presence on Rightmove, real estate agents lose mandates (listing instructions) from sellers, as they expect their property to be advertised on the largest platform in the country.

Value-added packages and marketing tools

To increase average revenue per customer (ARPA), Rightmove has developed a differentiated package structure. In addition to the basic listing, the company offers products designed to enhance differentiation:

Optimiser Edge: This is the current top-tier package for real estate agents (introduced in 2024). It offers features such as “Featured Property” (highlighting in search results), advanced branding options for the agency, and exclusive market data tools such as the “Premium Price Guide” to assist with valuation acquisition. In 2024, Rightmove saw the fastest adoption of this package in the company's history.

Ascend: A specialized premium package for developers (New Homes) that offers similar benefits in terms of visibility and data access.

Native Search Adverts: Advertising formats that blend seamlessly into search results, enabling agents to promote their brand to potential sellers in specific postcode areas.

Strategic Growth Areas (SGAs)

Rightmove is expanding beyond the pure listing business into adjacent areas of the value chain:

- Commercial real estate: A dedicated platform for office, industrial, and retail space aimed at investors and tenants.

- Mortgages: Digital mortgage brokerage. Users can obtain a “mortgage in principle” (mortgage certificate) directly on the platform. Rightmove acts as a lead generator for lenders and benefits from high user intent.

- Rental services: Products such as “Lead to Keys,” which digitize the entire rental process from inquiry to key handover and help brokers efficiently manage the flood of tenant inquiries.

- Data & valuation: Rightmove has the most comprehensive data set on the UK property market since 2002. This data is monetized in the form of automated valuations (AVM), market reports, and indices (House Price Index).

Target customers and motivation

Rightmove's customer base is purely B2B. Private individuals (sellers/landlords) cannot advertise directly on Rightmove, but must hire an estate agent. This protects the estate agents' business model and ensures their loyalty to Rightmove.

1. Estate agents

- Type: This group is the largest customer segment, comprising approximately 16,000 branches. It ranges from small, owner-operated individual offices to large national chains such as Connells or Countrywide, as well as online hybrid agents such as Purplebricks.

- Region: Nationwide coverage throughout the United Kingdom.

- Motivation: Getting mandates is the main source of motivation. In addition to finding buyers, agents use Rightmove to show sellers that they have the widest possible marketing reach. In a market where seller fees are the main source of income for agents, the “fear of missing out” (FOMO) in relation to Rightmove listings is the strongest sales driver. They also need efficiency tools to qualify leads, as the quality of inquiries is often more important than pure quantity.

2. New home developers

- Type: Large listed construction companies (e.g., Taylor Wimpey, Persimmon), regional developers, and housing associations.

- Segment: New construction projects, often sold off-plan (before completion).

- Motivation: Developers need to sell large volumes of units over long periods of time. They use Rightmove for branding and to generate interest early in the construction phase. Data on buyer demographics and price sensitivity is particularly valuable to them in order to market their projects optimally.

3. Commercial real estate professionals

- Type: Commercial brokers, institutional landlords, and asset managers.

- Motivation: To reduce vacancy rates for offices and warehouses. Rightmove's extensive reach is crucial for finding tenants, especially in the post-pandemic environment where office space is under pressure.

2. How Rightmove earns money

Revenue model and pricing

Rightmove operates according to a classic subscription model (similar to SaaS), which is supplemented by additional sales. The company generates most of its revenue not from transaction commissions on property sales, but from fixed monthly fees for the right to be present on the platform.

Revenue mechanics

- Membership fees (subscription fees): Each branch pays a monthly base fee. This fee grants access to the “Rightmove Plus” backend and the right to list an unlimited or limited number of properties.

- Package upgrades: In addition to the basic fee, Rightmove drives revenue through tiered packages (Essential, Enhanced, Optimiser). Higher packages include more branding tools and premium listings. The price difference is significant; the top package, “Optimiser Edge,” can cost around £1,500 per month and more, while basic packages are significantly cheaper.

- Add-ons: Customers can also purchase individual products such as “Premium Listings” or “Featured Property” on an ad hoc basis if they are not included in the package.

- Strategic growth areas:

- Commercial: Subscription model for commercial real estate agents.

- Mortgages: Here, Rightmove pursues more of an affiliate/lead generation model, generating revenue by referring mortgage prospects to banks or brokers.

- Data services: License fees for access to detailed market data for banks, appraisers, and authorities.

Pricing and pricing power

Rightmove's pricing has historically been opaque (“black box”). There is no public price list. Prices are negotiated individually based on the size of the broker, the region, and the package selected.

Pricing power: Rightmove has implemented annual price increases over the years that have often exceeded inflation. This has been possible because the cost to the estate agent is low relative to the value of a house sold, but the cost of not being present on Rightmove would threaten their existence.

Hybrid approach: While the core model is a fixed subscription, newer products in the areas of mortgages and tenant referencing introduce transaction-based elements, which still play a minor role in overall revenue.

Key revenue segments and shares (H1 2025)

Based on the half-year results for 2025, the revenue distribution is as follows:

| Segment | Revenue H1 2025 (£m) | Growth (YoY) | Share of total revenue | Analysis | |

|---|---|---|---|---|---|

| Agency | 150.8 | +9% | ~71% | The backbone of the company. Growth driven by upgrades to “Optimizer Edge” and price increases, less by new customers. | |

| New Homes | 37.5 | +11% | ~18% | Strong growth despite a difficult new-build market, as developers need to invest in marketing to secure sales. | |

| Other (incl. SGAs) | 23.4 | +18% | ~11% | Includes Commercial, Mortgages, Data Services, Overseas. The most dynamic segment with 37% growth in strategic areas. | |

| Total | 211.7 | +10% | 100% | Double-digit growth demonstrates the ongoing ability to monetize the platform. |

3. Quality of revenue

Predictability and recurrence

Rightmove's revenue quality can be classified as exceptionally high (investment grade).

- Recurring revenue: Since the majority of its revenue is based on monthly subscriptions, Rightmove has very high visibility of future cash flows. Unlike a pure transaction model (such as that of a traditional real estate agent), Rightmove's revenues do not immediately collapse when the real estate market stagnates. Real estate agents continue to pay their fees even in times of low transaction volumes in order to remain visible in the market and prepare for future business.

- Sticky customer base: Cancellation rates are minimal. Even in the difficult market environment of the first half of 2025, the retention rate among estate agents was 96%. This means that the customer base is extremely inert and loyal (or dependent).

Diversification and concentration

Segment concentration: There is a clear dependence on the UK residential real estate market and, in particular, on the solvency of real estate agents. A mass closure of real estate agencies (“branch closures”), for example due to a deep recession or the shift to purely online models without physical offices, would directly impact revenues, as the billing model is often “per branch.”

Economic dependence: Although the subscription model provides protection, Rightmove is not completely immune. However, during the 2008 financial crisis and the volatility of 2023/24, Rightmove demonstrated its ability to increase ARPA (average revenue per account) even when the absolute number of customers stagnated or declined slightly. In difficult times, estate agents tend to cut back on other marketing expenses (e.g., local newspapers, Google Ads) before canceling Rightmove.

New diversification: Commercial real estate and mortgages, which accounted for 11% of total sales, are growing at a strong rate (+107% in H1 2025) and are starting to lessen reliance on the residential brokerage industry alone.

4. Cost structure

Main cost factors

As a digital platform, Rightmove benefits from a lean cost structure with high operating leverage.

Personnel costs: This is the largest cost item. Rightmove employs highly specialized software developers, data analysts, and sales teams (account managers). The workforce grew by 14% to just under 900 employees in 2024, with 60% of new hires in the technology sector. In H1 2025, personnel costs accounted for around 60% of operating costs.

Marketing: A variable cost item that is currently being strategically expanded.

- To defend its market leadership against CoStar and keep the brand visible to consumers (“Search less, live more” campaigns), Rightmove is investing significantly in TV and digital advertising.

- Technology & infrastructure: Costs for servers, cloud hosting (migration to Google Cloud), and software licenses. These costs are increasing due to the modernization of the platform.

Margin profile

Rightmove has one of the most profitable profiles in the FTSE 100.

- Gross margin: Nearly 100%, as the marginal cost of an additional listing is negligible.

- Operating margin (underlying operating margin): Historically, this has often been above 74%. Currently (H1 2025 and FY 2024), it has stabilized at a level of 70-71%. Management has made a conscious decision to slightly reduce margins in favor of investments in growth and defense, but still maintain them at a globally leading level.

- Growth development: Due to scalability, each additional pound of revenue should contribute disproportionately to profit. However, the current investment cycle (AI, cloud) is temporarily dampening margins. The forecast assumes operating profit growth of 3-5% for the full year, which is below revenue growth, a sign of operational reinvestment.

Fixed costs vs. variable costs

The structure is fixed-cost-heavy (platform operation, salaries). Once these costs are covered (break-even is very low), profitability is enormous. This makes the company very profitable when revenue grows, but also vulnerable to margin pressure when revenue declines (negative operating leverage), which has hardly ever occurred to date.

5. Capital intensity

Assets and investment requirements

Rightmove is a classic asset-light model. There are no factories, inventories, or expensive machinery. The main assets are intangible: the brand, the software platform, the database, and the network effects.

Capital expenditure (capex)

Historically, capex requirements have been minimal (approx. 1-2% of revenue). This is currently changing strategically:

- Technological transformation: Rightmove is investing heavily in modernizing its tech stacks, including migration to the cloud and the integration of AI applications. A total of £60 million in investments is planned for the period 2026-2028, of which approximately £20 million will be capitalized. This project is expected to increase the capex share of revenue to up to 4%.

- Working capital: The need for working capital is low and often negative. Customers typically pay for their subscriptions in advance or promptly by direct debit, while Rightmove pays suppliers on credit terms. This process generates structural liquidity.

Cash conversion efficiency

Cash conversion is a highlight of the equity story.

6. Growth drivers

Rightmove has shifted its focus from pure volume growth (number of brokers) to value-added growth (revenue per broker).

1. ARPA increase (structural & long-term)

This is the most important lever. Since the number of real estate agencies in the UK is structurally limited and tends to stagnate or decline (consolidation), growth must come from price.

- Mechanism: Rightmove uses its pricing power to migrate customers to higher-value packages (“upselling”). The success of the “Optimizer Edge” package shows that real estate agents are willing to pay more for competitive advantages. In H1 2025, average revenue per advertiser (ARPA) increased by £112 (+7%) to £1,609.

- Price elasticity: So far, price increases have been well received. The limit is where costs exceed the economic benefits for the agent, which does not yet seem to have been reached given Rightmove's importance for winning mandates.

2. Product mix and innovation (structural)

- Digital products: The sale of add-on products such as “Local Homepage,” “Featured Agent,” and digital valuation tools contributes significantly to ARPA growth.

- AI and data: New AI-powered tools for identifying potential sellers and automated lead qualification offer further upsell potential.

3. Strategic growth areas (structural)

- Mortgages: The market for digital mortgage brokerage is huge. Rightmove is attempting to position itself earlier in the customer journey (during the financing review, not just when searching for property). With revenue growth of 107% in H1 2025, this area is showing tremendous traction.

- Commercial: Rightmove is increasingly establishing itself as the standard for commercial real estate as well, consolidating a previously fragmented market segment.

4. Volume (Cyclical)

- A resurgence in real estate transactions in the UK (driven by falling interest rates and improved affordability) would increase the number of new home developments and strengthen the solvency of estate agents, indirectly supporting membership growth. In H1 2025, membership rose slightly by 1%, indicating stabilization.

7. Competitive advantages

Rightmove has one of the broadest and deepest economic moats on the European stock market.

1. Network effects

This is the strongest protective barrier.

- Mechanism: The more properties listed on Rightmove, the more buyers use the platform. The more buyers use the platform, the more indispensable it becomes for sellers (and their agents).

- Dominance: Rightmove controls over 80-86% of the time consumers spend on the top real estate portals. Even if competitors such as Zoopla or OnTheMarket have listings, they lack the critical mass of user attention (“eyeballs”) to generate the same value for agents.

- Self-reinforcing loop: Users have developed the habit of “looking on Rightmove.” This mental availability is extremely difficult to break.

2. High switching costs (Switching Costs)

- For estate agents, the switching costs are economic in nature. An estate agent who leaves Rightmove to save on fees risks no longer receiving sales instructions from owners, as they expect their property to be listed on the largest website in the country. The risk of lost revenue far outweighs the cost savings.

3. Brand

- Rightmove is practically synonymous with property searches in the United Kingdom. Aided brand awareness is over 90%.6 Much of the traffic (approx. 85%) comes directly (“direct traffic”) or via organic search, which means that Rightmove—unlike many of its competitors—does not have to pay for customer traffic every time (low traffic acquisition costs).

Verifiability of the advantage

The sustainability of this advantage is reflected in the financial figures:

- Operating margins: Consistently >70%, even with increasing competition.

- Retention: 96% customer loyalty despite price increases.

- ROIC: Extremely high returns on capital, as hardly any capital is required for growth.

8. Industry structure and position

Value chain and sources of profit

The online real estate advertising (“classifieds”) industry occupies a profitable position in the value chain. It aggregates fragmented supply (thousands of real estate agents) for fragmented demand (millions of searchers). Value is created through efficient matching. Since real estate transactions are high-value, agents are willing to pay high marketing fees to earn commissions (typically 1-2% of the property value).

Market structure: oligopoly with a dominant leader

The UK market is consolidated:

- Rightmove: The clear market leader (“price setter”).

- Zoopla: Number 2, strong in data (Hometrack) and software, but lagging significantly in user retention.

- OnTheMarket (now CoStar): Number 3, originally founded by brokers as a counterweight to the duopoly and now acquired by CoStar.

The CoStar disruption

The acquisition of OnTheMarket by the US-based CoStar Group in 2023 for £100 million has changed the market structure.

The challenger: CoStar is a giant with a market capitalization of approximately $33 billion and deep pockets.

Strategy: CoStar has announced that it will invest £46.5 million in marketing in the first year – about three times Rightmove's historical marketing budget. The goal is to massively increase traffic and make OnTheMarket number 1, similar to what CoStar is attempting to do in the US with Homes.com.

Current status: CoStar reports aggressive growth rates (traffic +82% in Q3 2024) and claims to have overtaken Zoopla in traffic.

Rightmove's position: Rightmove is acting as the defender. It is no longer the undisputed monopolist in “sleep mode,” but must actively invest to maintain its market share and pricing power. Nevertheless, Rightmove remains the price setter; brokers often use OnTheMarket in addition (multi-homing), but do not cancel Rightmove.

9. Unit economics and key KPIs

Rightmove's unit economics are exceptionally attractive, but indicate the need for price increases amid stagnant volume.

| KPI | Value (H1 2025 / FY24) | Trend (YoY) | Analysis | |

|---|---|---|---|---|

| ARPA (total) | £1,609 / month | +7% | The key growth driver. Shows that brokers are willing to pay ~£100 more per month annually. | |

| ARPA (New Homes) | £2,093 / month | +8% | Developers pay significantly more than agents as their marketing budgets per unit are higher. | |

| Membership (Branches) | 19,323 | +1% | Stabilization after slight declines. Shows that the market is saturated; growth via volume is limited. | |

| Churn | ~0.8% p.m. (implied) | Declining | Extremely low for B2B SaaS. Retention of 96% 1 is a best-in-class figure. | |

| Consumer time | 9.1 billion minutes (H1 25) | Rising | Most important indicator of network effect. As long as this value rises, the value for brokers remains intact.1 | |

| LTV / CAC | Very high | Stable | Since traffic is organic, customer acquisition costs (CAC) are low. The lifetime value (LTV) of a broker is enormous, as they stay for decades and accept price increases. |

Development: Unit economics are improving in monetary terms (higher ARPA), but usage intensity (time on site) must be defended against aggressive competition from CoStar.

10. Capital allocation and balance sheet

Historical capital allocation

Rightmove has established a disciplined and shareholder-friendly capital allocation policy based on three pillars:

- Organic reinvestment: Priority is given to the business itself. Due to the asset-light model, only small amounts have historically been required for this. This is now changing slightly due to increased tech investments.

- Progressive dividend: Rightmove aims to increase its dividend in line with profit growth. In H1 2025, the dividend was increased by 9% to 4.05p.

- Share buybacks: Surplus capital not required for 1. and 2. is used for buybacks. Rightmove has repurchased a significant portion of its outstanding shares over the last decade (reducing the number of shares from 819 million to 795 million in 2023 compared to 2024 alone). In H1 2025, £112.4 million was returned to shareholders.

Balance sheet strength

Debt: The balance sheet is immaculate. Rightmove is debt-free. As of June 30, 2025, the company had £42.4 million in cash and no interest-bearing financial liabilities.

Liquidity: Due to high cash conversion, liquidity is assured at all times. There are no significant off-balance sheet commitments.

- Value creation: Capital allocation has created massive value. ROIC (return on invested capital) is in the triple digits (often >400%) as capital employed is minimal and profits are extremely high. Buybacks have leveraged EPS growth.

Takeover bid

In September 2024, the board rejected a takeover bid from Australia's REA Group, which valued the company at £6.2 billion (approx. 780p per share).

The rejection was justified on the grounds that the offer “fundamentally undervalued” the company. Given the current share price (~510p), management is under pressure to prove that this decision was in the best interests of shareholders and that the intrinsic value is indeed higher.

11. Risks and sources of error

Despite its strong position, Rightmove's risk profile is higher today than it has been in the last ten years.

1. Competitive risk (existential threat from CoStar)

The biggest risk is that CoStar, with its deep pockets (budget surplus), will break Rightmove's network effect. If OnTheMarket attracts enough users through massive advertising (“traffic parity”), brokers could start to view Rightmove as “optional.” Underestimating CoStar's tenacity is a possible source of error. If Rightmove loses market share, its pricing power will collapse, leading to a massive de-rating.

2. Technological risk (disruption of search)

Generative AI (ChatGPT, Perplexity) is changing how people search. If users start dictating their real estate needs to an AI bot instead of scrolling through listings on Rightmove, Rightmove could be downgraded to a pure data commodity and lose its direct customer relationship (interface). Rightmove is responding with its own AI investments, but the risk of disruption to its “listings for a fee” business model remains.

3. Macroeconomic risks

A prolonged slump in the real estate market could lead to a wave of consolidation among real estate agents. Fewer real estate agencies mean fewer subscriptions. Rightmove cannot increase ARPA indefinitely if its customer base shrinks and its profitability declines.

4. Regulatory risk

As a market-dominating company, Rightmove is under scrutiny by the competition authorities (CMA). Measures against product bundling or pricing could adversely affect the business model.

12. Valuation and expected return profile

Current valuation (as of January 2026)

- Share price: ~506p - 515p.

- Market capitalization: ~£3.9 billion

- P/E ratio: Approx. 19-20x (based on estimated EPS of ~26p for 2025).

- Comparison: Historically, Rightmove has often traded at a P/E ratio of >25x to 30x. The current discount reflects uncertainty regarding CoStar and the rejected REA offer. Compared to global peers such as REA Group (often >30x) or Scout24, Rightmove is “cheaper” if you believe in the robustness of the model.

- FCF yield: With a cash conversion of >100%, the P/E ratio corresponds to a free cash flow yield of approximately 5.0–5.5%. This is an attractive base yield, to which growth is added.

Scenario framework

| Scenario | Probability | Assumptions | Implied value (approx.) | |

|---|---|---|---|---|

| Bear Case | 20% | CoStar gains >20-30% market share in traffic. Rightmove must lower prices or massively increase marketing (margin falls to <55%). Growth stagnates. | < 380p De-rating to “ex-growth” multiple (12-14x). |

|

| Base Case (Base) | 50% | Rightmove defends its position (traffic share remains >75%). ARPA continues to grow at 5-8%. Margin stabilizes at 68-70%. SGAs deliver additional growth. | 550p - 620p Solid returns through EPS growth (6-8%) plus dividends/buybacks (5%). Multiple stable at ~20x. |

|

| Bull Case | 30% | CoStar attack fizzles out, OnTheMarket remains far behind. Mortgage division scales massively. Market realizes that REA offer was fair. M&A fantasy returns. | > 750p Return to historical multiples (25x) and approach to takeover price of 780p. |

Conclusion

The current price of ~510p (approx. EUR 5.80) appears fair to attractive. It already factors in a considerable degree of skepticism regarding the CoStar threat. If Rightmove proves that its moat holds (as suggested by data from H1 2025), there is significant upside potential (“re-rating”).

13. Catalysts and time horizon

Short-term catalysts (6-12 months)

- Half-year and annual results: Investors will be paying close attention to whether the operating margin of 70% is maintained and whether ARPA continues to grow. Any signs of weakness would be punished.

- CoStar news flow: Reports on the success or failure of OnTheMarket's marketing campaigns. If CoStar signals that customer acquisition is more expensive than planned, Rightmove shares will breathe a sigh of relief.

Slow-acting catalysts (1-3 years)

- Tech transformation: The completion of cloud migration and the introduction of new AI products by 2026/2027 could increase efficiency and open up new sources of revenue, allowing margins to expand again.

- M&A return: The rejected REA offer showed that strategic buyers value Rightmove more highly than the market. If the share price continues to languish, REA could return or a private equity consortium could make an offer.

Resources

- Half Year Results 2025 - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/07/Rightmove-H1-25-Presentation.pdf

- Half-year Report - 07:00:07 July 24, 2025 - RMV News article | London Stock Exchange, accessed January 9, 2026, https://www.londonstockexchange.com/news-article/RMV/half-year-report/17151476

- 251106 RNS Trading Update - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/11/251106-RNS-Trading-Update.pdf

- ‘AI ready’ Rightmove reveals rising estate agent revenues - The Negotiator, accessed January 9, 2026, https://thenegotiator.co.uk/news/proptech/newly-ai-ready-rightmove-reveals-rising-estate-agent-revenues/

- Rightmove plc, the UK's largest property portal, today announces its audited results for the year ended December 31, 2024, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/02/FY24-Full-RNS.pdf

- Full Year Results - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/03/250228-FY24-Presentation-vF.pdf

- Fuel your success with Optimiser Edge - Rightmove Hub, accessed January 9, 2026, https://hub.rightmove.co.uk/optimiser-edge/

- Premium Price Guide - Rightmove Hub, accessed January 9, 2026, https://hub.rightmove.co.uk/premium-price-guide/

- Half Year Results - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2024/07/H1-2024_Presentation_Rightmove.pdf

- Rightmove Reports Strong H1 2025; 10% Revenue Rise And Strategic Growth, accessed January 9, 2026, https://www.directorstalkinterviews.com/rightmove-reports-strong-h1-2025-10-revenue-rise-and-strategic-growth/4121209224

- Strong results and product delivery across the platform - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/07/H1-2025-RNS.pdf

- Q1 2025 Tracker | Commercial Property News - Rightmove, accessed January 9, 2026, https://www.rightmove.co.uk/commercial-property/news/q1-2025-tracker/

- title“ content=”Property Listings with Rightmove - Drop Cowboy, accessed January 9, 2026, https://www.dropcowboy.com/uk/bulk-sms/rightmove

- H1 2024 - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2024/07/240725-Rightmove-H1-RNS.pdf

- Investor Update | Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/11/Rightmove-Investor-Update-2025.pdf

- Annual report and accounts 2024 - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2025/05/RIG001_2024AR_WEB_250321_160525.pdf

- Rightmove shares tumble but is its property portal dominance now under threat?, accessed January 9, 2026, https://propertyindustryeye.com/rightmove-shares-tumble-following-costars-accepted-bid-for-onthemarket/

- CoStar Group Offers to Acquire Leading UK Residential Property Portal OnTheMarket, accessed January 9, 2026, https://www.costargroup.com/press-room/2023/costar-group-offers-acquire-leading-uk-residential-property-portal-onthemarket

- Costar Group Completes Acquisition of OnTheMarket.com With Overwhelming 97% Shareholder Support, accessed January 9, 2026, https://www.costargroup.com/press-room/2023/costar-group-completes-acquisition-onthemarketcom-overwhelming-97-shareholder

- 2024 for OnTheMarket, accessed January 9, 2026, https://www.onthemarket.com/content/2024-for-onthemarket/

- UK Roundup: Rightmove, Zoopla And OnTheMarket All Make Announcements, accessed January 9, 2026, https://www.onlinemarketplaces.com/articles/uk-roundup-rightmove-zoopla-and-onthemarket-all-make-announcments/

- REA Withdraws Its Bid for Rightmove After Multiple Rejections, Share Price Plummets, accessed January 9, 2026, https://www.mpamag.com/uk/news/general/rea-withdraws-its-bid-for-rightmove-after-multiple-rejections-share-price-plummets/507738

- Rejection of Possible Offer Following Engagement with REA - Rightmove Plc, accessed January 9, 2026, https://plc.rightmove.co.uk/content/uploads/2024/09/Statement-re-Rejection-of-possible-offer-following-engagement-with-REA.pdf

- Rightmove plc Share Price (RMV) Ord GBP 0.001 - Hargreaves Lansdown, accessed January 9, 2026, https://www.hl.co.uk/shares/shares-search-results/r/rightmove-plc-ord-gbp-0.001

- Rightmove Plc Share Price History - Historical Data for RMV - ADVFN UK, accessed January 9, 2026, https://uk.advfn.com/stock-market/london/rightmove-RMV/share-price-history